College Savings Plans: 529 Pros and Cons

Funding a college education constitutes a significant financial commitment. If you're contemplating the idea of establishing a 529 plan for a child or grandchild, it's crucial to grasp the intricacies of 529 plan regulations and their operational principles. This compilation of advantages and disadvantages associated with 529 plans will assist you in making an informed decision regarding your child's college savings.

LIFE INSURANCESTRATEGYCOLLEGE SAVING529 PLANS

Legacy Retirement

9/29/20234 min read

Funding a college education constitutes a significant financial commitment. If you're contemplating the idea of establishing a 529 plan for a child or grandchild, it's crucial to grasp the intricacies of 529 plan regulations and their operational principles. This compilation of advantages and disadvantages associated with 529 plans will assist you in making an informed decision regarding your child's college savings.

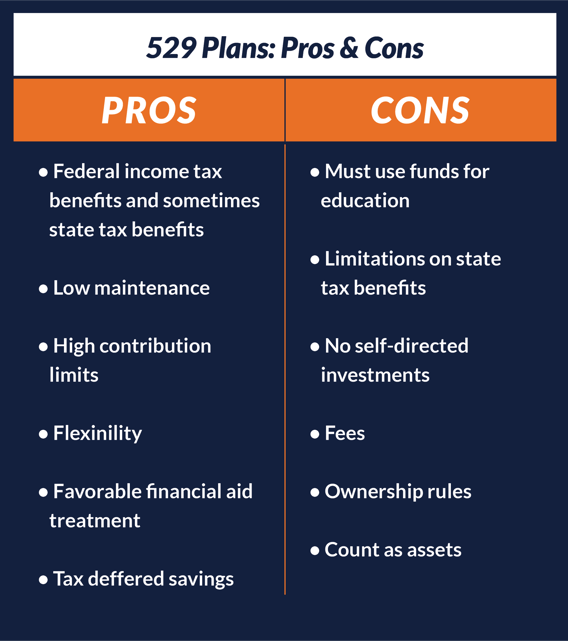

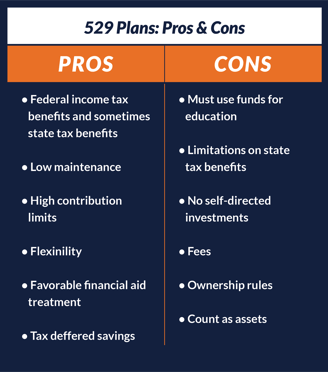

Let's delve into the strengths of 529 plans, beginning with their numerous advantages: The Pros

Tax Benefits: Investing in a 529 plan yields various tax advantages. These plans facilitate tax-deferred growth on investments, and when funds are used for qualified educational expenses—covering college tuition, fees, books, supplies, certain room and board costs, up to $10,000 annually for K-12 tuition, and up to $10,000 per beneficiary and per sibling for student loan repayment—the distributions become tax-free. Beginning in 2024, beneficiaries can also transfer up to $35,000 tax-free to a Roth IRA in their names, subject to specific limitations.

In most instances, states exempt qualified 529 plan distributions from taxable income, and many states offer state income tax deductions or credits for contributions to these plans. Notably, 529 plans are the sole college savings vehicle offering state tax benefits. While some states may require residency for tax benefits, families typically have the freedom to choose a 529 plan from any state, except when opting for a prepaid tuition plan.

Low Maintenance: Opening a 529 plan account is a hassle-free process, accomplished online or through a licensed financial advisor. Families who prefer an "auto-pilot" approach can opt for automatic investment plans linked to their bank accounts or payroll deductions. The ongoing investment management within a 529 plan is expertly handled by the program manager.

High Contribution Limits: Unlike other savings plans like Roth IRAs or Coverdell Education Savings Accounts, 529 plans impose no annual contribution limits and offer substantial aggregate limits. Maximum aggregate limits vary by state, ranging from $235,000 to $529,000.

Contributions to 529 plans are regarded as completed gifts to the designated beneficiary for tax purposes. In 2022, up to $16,000 qualifies for the annual gift tax exclusion, and there's an option to contribute as much as $80,000 in a single year without triggering a taxable gift, treating the contribution as if it were spread over five years.

Favorable Financial Aid Treatment: When a dependent student's parent or the dependent student themselves owns a 529 plan, it is reported as a parental asset and has a relatively minimal impact on financial aid eligibility. Distributions from accounts owned by other family members or loved ones do not count as income on the Free Application for Federal Student Aid (FAFSA).

Flexibility: 529 plans extend their benefits universally, regardless of household income or contribution amount. You can invest in nearly any 529 plan, irrespective of your residence or your child's intended college location.

529 Plans Pros and Cons

Drawbacks of the 529 Plan for College Savings: The Cons.

Penalty for Non-Qualified Withdrawals: Withdrawals that do not meet the criteria for qualified educational expenses incur income tax and a 10% penalty on the earnings portion of the distribution. Some exceptions exist, such as if the beneficiary receives a scholarship, attends a U.S. Military Academy, passes away, or becomes disabled.

State Income Tax Recapture: If an account owner performs a rollover into another state's 529 plan, any state income tax deductions and credits previously claimed may be subject to recapture, and the earnings portion of the rollover may be added back to the state's taxable income.

Limited Investment Choices: 529 plan account owners must make their investment selections from a predetermined menu of options provided by the plan. Typically, this includes static investment portfolios with defined risk levels, individual fund portfolios, and age-based portfolios that automatically adjust asset allocation as the beneficiary approaches college age.

Fees: Higher 529 plan fees translate to reduced savings for college. Direct-sold 529 plans generally entail lower costs compared to advisor-sold plans, but expenses can also fluctuate among different 529 plan portfolios. Thorough research is vital to identify a low-cost 529 plan option that aligns with your college savings objectives.

Ownership Rules: In a 529 plan, the account owner, not the beneficiary, possesses legal control over the account funds. This means the account owner can change the beneficiary at will or, in a more detrimental scenario, take a non-qualified distribution and liquidate the plan. This could pose challenges if a parent relies on a grandparent or another relative's 529 plan to fund their child's college education.

Is a 529 plan the Right Choice for You?

To determine if a 529 plan aligns with your needs, consider the following factors when weighing the pros and cons:

Intended Use for Educational Savings: Are you exclusively planning to use the funds for educational expenses? 529 plans are designed for this purpose; diverting funds elsewhere may incur penalties.

Savings Goals: Determine how much you need to save, whether it's for college, graduate school, K-12 education, or apprenticeships.

Residency: Consider your state of residence. Some states offer additional tax benefits for 529 plans, although this is limited to specific regions.

While 529 plans offer substantial tax advantages, high contribution limits, and a relatively modest impact on financial aid, it's essential to carefully assess your individual circumstances to determine if this savings vehicle suits your educational financing objectives.

College Saving Best Kept Secret: The 529 Alternative

Permanent life insurance policies, such as whole life or universal life insurance, have a cash value component that grows over time. You can consider these policies as a form of forced savings. As you pay premiums, a portion of those premiums goes into the cash value account, which earns interest or investment returns over the years. You can use the cash value to fund college expenses by taking out a loan on the cash value of you policy. You can either maintain the life insurance, lower your monthly premium or stop paying it altogether. As long as the policy has a cash value it will fund itself.

Pros:

Guaranteed cash value growth.

Tax-free death benefit with living benefit options.

You can take out loans against the cash value without triggering immediate taxes, which can be used for college costs.

Pay back your loans with the death benefit, your beneficiary will get the death benefit less the interest and loan amount.

Does not count as an asset.

Life coverage during college saving and college attendance years.

Cons:

Higher premiums compared to term life insurance.

Lower returns on investment compared to other investment options.

Reduces the death benefit if you withdraw too much cash value.