When Can I Retire FROM FERS?

How Is MY FERS Retirement Calculated?

Can I Count Military Service Toward FERS Retirement?

What's the Role of the Thrift Savings Plan (TSP)?

What Health Benefits Are Available in Retirement?

How does Social Security work with FERS?

Are there Special FERS Retirement Provisions for HIGH RISK EMPLOYEES?

What are the Survivor Benefits Under FERS?

Does FERS have special disability retirement options?

Where can I find help to plan for my retirement from FERS?

Your Top 10 FERS Questions Answered

Click a Topic Below:

Voluntary, immediate retirement

Under the Federal Employees Retirement System (FERS), the eligibility age for retirement varies depending on your birth year and years of service. It's important to note that while you might be eligible for early retirement at a Minimum Retirement Age (MRA), the amount of your annuity will depend on factors like your length of service and highest three years of average salary. Additionally, retiring earlier than your Normal Retirement Age (NRA) may result in a reduction in your annuity. There are five categories of benefits in the Federal Employees Retirement System (FERS) Basic Benefit Plan:

Voluntary/Immediate Retirement

Early Retirement

Deferred Retirement

Disability Retirement

Phased Retirement

When can I retire from the FERS?

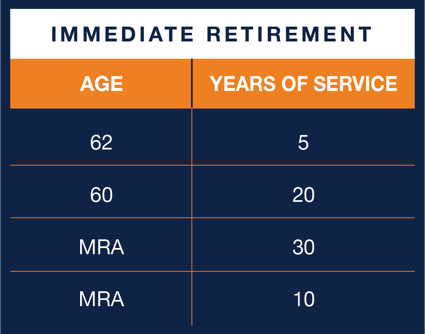

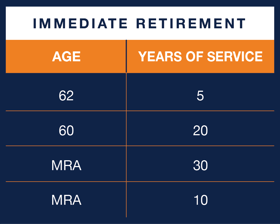

An immediate retirement benefit is one that starts within 30 days from the date you stop working. If you meet one of the sets of age and service requirements on the "IMMEDIATE RETIREMENT" chart, you are entitled to an immediate retirement benefit. If you retire at the MRA with at least 10, but less than 30 years of service, your benefit will be reduced by 5 percent a year for each year you are under 62, unless you have 20 years of service and your benefit starts when you reach age 60 or later.

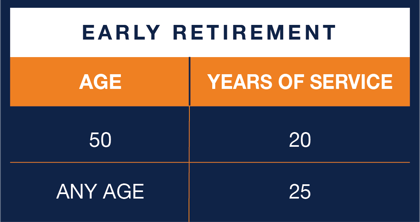

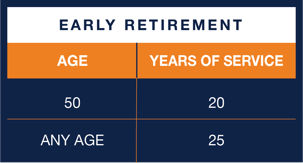

Early retirement

The early retirement benefit is available in certain involuntary separation cases and in cases of voluntary separations during a major reorganization or reduction in force. To be eligible, you must meet the requirements on the "EARLY RETIREMENT" chart.

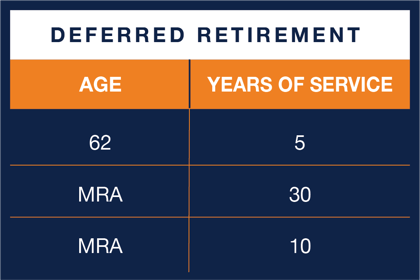

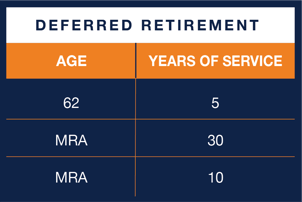

Deferred retirement

Deferred refers to delayed payment of benefit until certain criteria are met. For example, if you leave Federal service before you meet the age and service requirements for an immediate retirement benefit, you may be eligible for deferred retirement benefits. To be eligible, you must have completed at least 5 years of creditable civilian service. You may receive benefits when you reach one of the required ages on the "DEFERRED RETIREMENT" chart. If you retire at the MRA with at least 10, but less than 30 years of service, your benefit will be reduced by 5 percent a year for each year you are under 62, unless you have 20 years of service and your benefit starts when you reach age 60 or later.

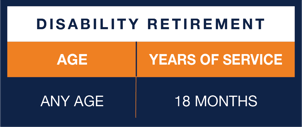

Disability retirement

You must have have at least 18 months of service and become disabled, while employed in a position subject to FERS, because of a disease or injury, for useful and efficient service in your current position. The disability must be expected to last at least one year. Your agency must certify that it is unable to accommodate your disabling medical condition in your present position and that it has considered you for any vacant position in the same agency at the same grade/pay level, within the same commuting area, for which you are qualified for reassignment.

Phased retirement

Phased Retirement allows full-time employees to work part-time schedules while beginning to draw retirement benefits. This will allow managers to better provide training opportunities for new employees from highly experienced employees that are transitioning to full retirement.

In Phased Retirement you will continue to accrue "Years of Service", although the maximum time allowed is currently 6 months. On average, employees enrolled in Phased Retirement work around 20 hours per week. Once your Phased Retirement period ends and you enter full retirement, your Years of Service and cost of living adjustments will be applied, your monthly benefit is then adjusted to reflect the additional time working. For a more in-depth discussion of Phase retirement, see our article, "What is Phased Retirement?"

Click to enlarge MRA Chart

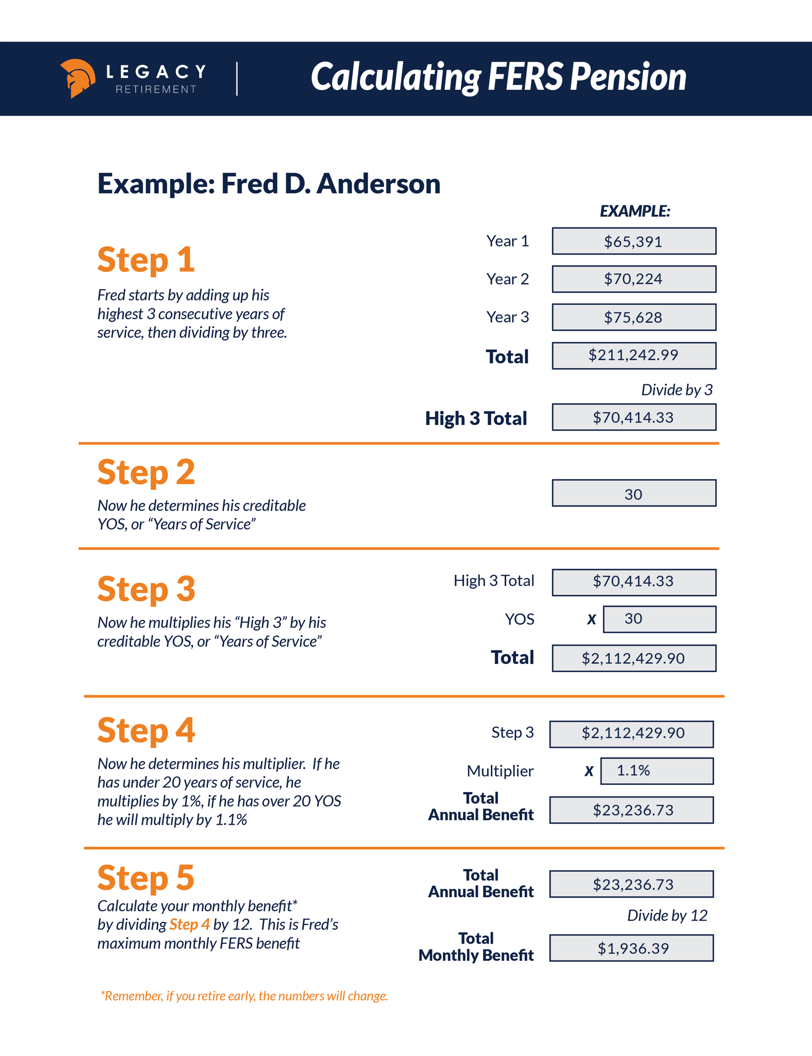

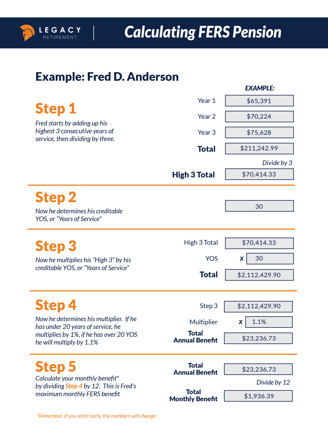

FERS basic annuity calculation & options

Your basic annuity is based on your length of service and the highest average basic pay you earned during any 3 consecutive years of service, also known as your “high-3”. These three years are usually your final three years of service, but can be an earlier period, depending on your circumstances. To determine your length of service, add all your periods of creditable service, then eliminate any fractional part of a month from the total.

Your basic pay includes increases to your salary for which retirement deductions are withheld, such as shift rates. It does not include payments for overtime, bonuses, etc.

How Is my FERS retirement calculated?

CODE K - FERS Traditional: Employees hired between January 1, 1987 and December 31, 2012. Your pension is designed to make up 20-30% of your working salary. Your Social Security is also designed to replace around 20-30% of your working salary. Your TSP funds are designed to help fill the rest of your income needs in retirement. Every paycheck you contribute .8% towards your FERS Pension and 6.2% towards Social Security. At retirement you will select one of three retirement options:

Option 1 (Unreduced/Maximum): This option pays for your life ONLY. Once you die there is no payout to a beneficiary, regardless of the balance of your annuity.

UNDER 20 Years of Service - Highest 3 consecutive years of salary x Years Of Service x 1% = Your Annual Benefit

OVER 20 Years of Service - Highest 3 consecutive years of salary x Years Of Service x 1.1% = Your Annual Benefit

Option 2 (Maximum/Survivor): This option involves electing a beneficiary that would receive your FERS benefit should you predecease them. This option will cost 10% of your maximum benefit as long as you are alive.

Example: (Max benefit ) $20,000/yr - 10% ($2,000) = $18,000 reduced to pay for

your beneficiary

If you die your beneficiary will received 50% of your maximum benefit for the rest of their life.

Example: (Max benefit ) $20,000/yr / 2 =

$10,000 annual benefit

Option 3 (Partial/Survivor): This option involves electing a beneficiary that would receive your FERS benefit should you predecease them. This option will cost 5% of your maximum benefit as long as you are alive.

Example: (Max benefit ) $20,000/yr - 5%

$1,000) = $19,000 reduced to pay for

your beneficiary

If you die your beneficiary will received 25% of your maximum benefit for the rest of their life.

Example: (Max benefit ) $20,000/yr / 4 =

$5,000 annual benefit

The computation of benefits can vary greatly depending on your personal circumstances and which of the 3 retirement options you choose. In this overview we will cover some basic computations for Code K, traditional FERS members. However if your circumstances are not listed below it is recommended that you schedule an appointment with a certified Federal Retirement Consultant (FRC). You can also consult the official OPM guidelines. However you may still want to ask for assistance from an FRC.

Click to enlarge the FERS Pension calculation Example

Here's how it generally works:

Yes, military service can be counted towards your Federal Employees Retirement System (FERS) retirement, for a fee. If you have performed honorable active duty military service, you may be eligible to make a deposit to your FERS retirement account to receive credit that will be used to calculate your total years of service (YOS).

Remember to gather all necessary documentation of your military service, such as your DD-214 form, to provide as evidence when processing the military service credit deposit.

Can I count military service towards FERS retirement?

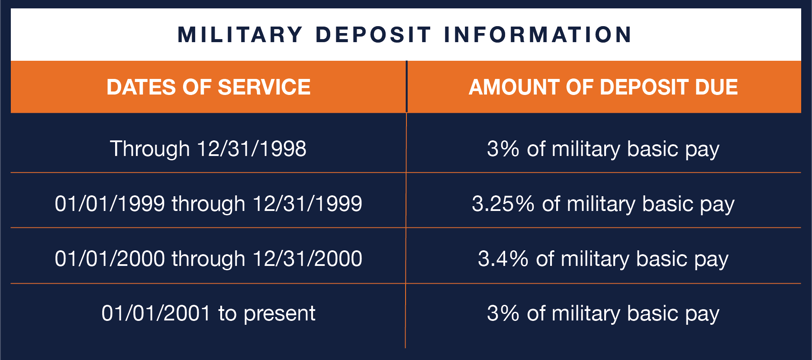

Military Service Credit Deposit: To count your military service towards your FERS retirement, you will need to make a deposit into your FERS retirement account. The deposit for military service credit in the Federal Employees Retirement System (FERS) is actual money that you need to pay to receive credit for your military service towards your federal civilian retirement.

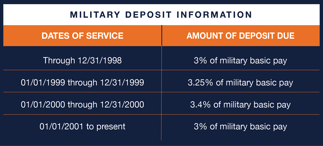

What is the Deposit For?: The deposit represents the contributions you would have made to your FERS retirement account if you had been employed by the federal government during the time you served in the military. This deposit is typically a percentage of your military pay during the time of your service. The specific percentage varies depending on when you performed your military service. (See chart below)

Eligibility: In order to be eligible to make a deposit for your military service, you must have been honorably discharged from the military and have a civilian federal service appointment.

Impact on Retirement Benefits: Once you make the deposit and the military service is credited, it will factor into your total years of service used to calculate your FERS retirement benefits. This could potentially increase your length of service and, consequently, the amount of your retirement benefit.

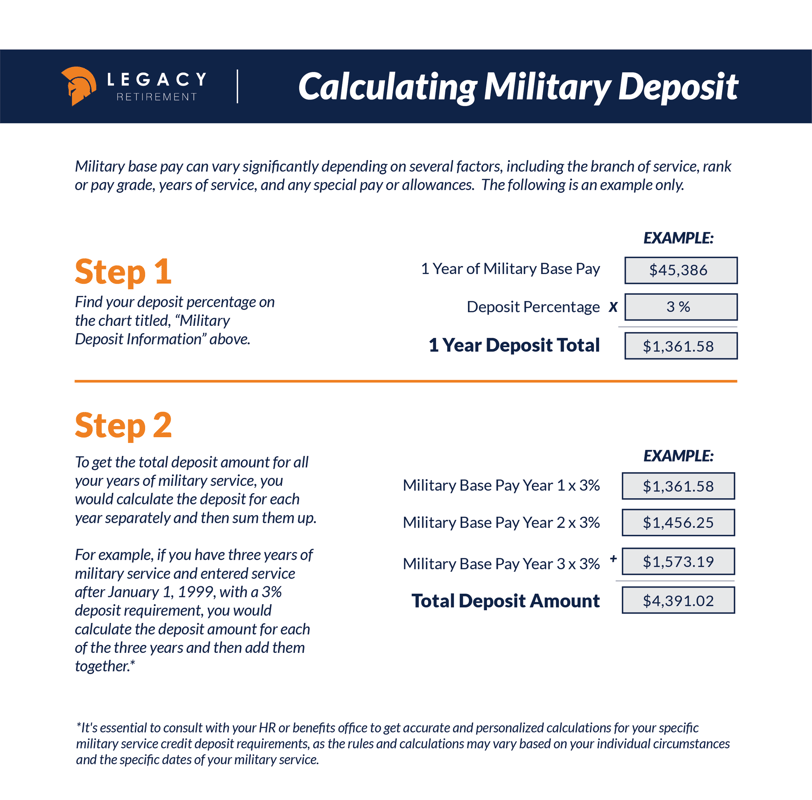

Calculation: The way your military service affects your FERS annuity calculation depends on various factors, including the length of your military service and the timing of your deposit. Military service credit can affect both your length of service calculation and your High-3 Average Salary calculation, which are important components of your FERS annuity.

Click on the "Calculating Military Deposit" chart to enlarge

Click on the "Military Deposit Information" chart to enlarge

Primary roles and features of the Thrift Savings Plan (TSP):

The Thrift Savings Plan (TSP) is a retirement savings and investment plan for federal employees and members of the uniformed services, including the Army, Navy, Air Force, Marine Corps, Coast Guard, and certain other federal agencies.

It is designed to help participants save and invest for their retirement years. The TSP is a key component of the retirement benefits offered to federal employees and service members. Federal employees have the opportunity to save part of their income for retirement, receive matching agency contributions and reduce their current taxes.

What is the role of the Thrift Savings Plan (TSP)?

Portability: If you leave federal service, you can keep your TSP account active and continue to manage and contribute to it. You can also roll over your TSP balance into an eligible IRA or another employer's retirement plan.

Low Costs: The TSP is known for its extremely low administrative costs and investment fees, making it an attractive option for retirement savings.

Access to Funds: While the primary purpose of the TSP is retirement savings, there are certain circumstances (such as financial hardship, age 59½ or meet the minimum retirement age and minimum years of service requirements) that allow for penalty-free withdrawals, although since the funds are tax-qualified (Meaning you didn't pay taxes on the income yet) you will be required to pay taxes once funds are withdrawn. The exception would be if your TSP funds were allocated in a Roth account or you are rolling the funds into a different tax-qualified account like an IRA, 403(b), 457(b) etc.

Consistency and Long-Term Focus: The TSP encourages a disciplined approach to retirement savings by automating contributions from your paycheck. Its investment options are designed to support long-term growth and retirement planning.

Education and Resources: The TSP provides educational materials, resources, and tools to help participants understand their investment options, make informed decisions, and plan for retirement. Federal employees can gain the most benefit from meeting with a certified FRC (Federal Retirement Consultant). FRC's can provide a full benefit analysis that shows all or your FERS, SS, TSP and other investments combined in one report. They can then recommend a plan based on your personal goals and circumstances. This is nearly always a free service. The publishers of this website can provide more information if desired. Click here to set a free consultation with a Legacy Retirement agent.

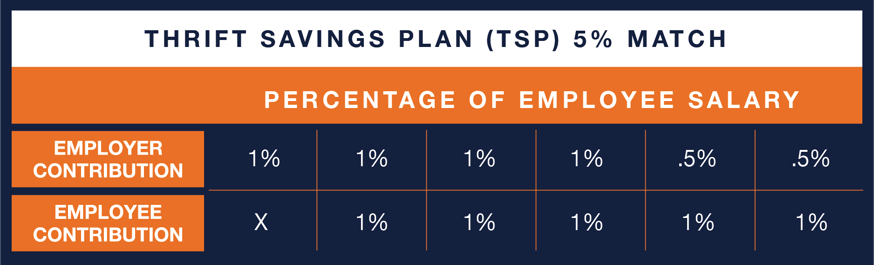

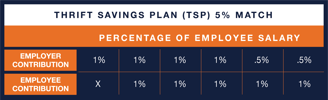

Employer Matching (for Some Participants): Some federal agencies and military branches offer employer matching contributions for their employees' TSP contributions. The matching policy varies by agency and service branch. Generally there is a true match up to 5% of your contribution - free money! (Not applicable for CSRS employees) The great news is that you will get TSP Statement whether you contribute or not - because your employer puts in 1% of your salary no matter what! Whether the 1% contribution from your employer is enough to fund your retirement will depend o your personal circumstances. However, the matching element of the TSP is a huge advantage for participants and an excellent way to create a 3rd source of retirement income. This chart should help make sense of how the match works:

G-FUND: This fund is typically government securities, the least amount of risk making it nearly a cash account. Statistically, a little over 50% of all TSP accounts are in the G-Fund.

F-FUND: The F-Fund is an investment fund. It focuses on fixed-income securities, specifically bonds. F-Fund is designed to provide stability and income through bonds, making it generally less volatile than equity-based funds. However, it is subject to market risks, interest rate changes, and economic conditions that can impact it's performance.

C-FUND: The C-Fund is designed to provide participants with exposure to the U.S. stock market, specifically tracking the performance of the Standard & Poor's 500 (S&P 500) Index. The S&P 500 is a measuring tool. It helps us understand how well the 500 biggest and most important companies in the United States are doing.

The performance of the C Fund is directly tied to the performance of the S&P 500 Index. If the index goes up, the C Fund's value generally increases; if the index goes down, the C Fund's value generally decreases. The C-Fund is typically suited for participants with a long-term investment horizon, such as those who are early in their careers and have many years until retirement.

S-FUND: The S-Fund is designed to provide participants with exposure to small and mid-sized U.S. companies and track the performance of the Dow Jones Stock Market Index. The Dow Jones is like the S&P 500, only it tracks the performance of a small group of 30 big, well-known companies. These companies are leaders in their industries. It's an older index, however it is one of the most recognized indicators of the stock market's performance.

As the index goes up or down, the value of the S-Fund generally follows suit. It is typically suited for participants with a long-term investment horizon, such as those who are early in their careers and have many years until retirement.

I-FUND: The I-Fund is designed to provide participants with exposure to international stocks and track the performance of the MSCI EAFE Index. The MSCI EAFE is a widely recognized tool that measures the performance of markets in developed countries located in Europe, Australasia & the Far East (EAFE). is generally suited for participants with a longer investment horizon who are willing to accept the potential for higher returns along with greater risk.

L-FUND (Lifecycle): L-Funds are designed for participants who prefer a more automated approach to investing. Participants simply choose the L-Fund that corresponds to their expected retirement date, and the fund automatically adjusts its allocation over time. Allocation means deciding how much of your investment money you'll put into the different TSP fund types. (For example you may want 50% in the G, 20% in F, 10% in each C, S & I). The idea is to create a balanced plan that suits your goals and needs. If you choose a Lifecycle Fund (L-Fund) The percentage of your investments will start off with more market exposure, then get less and less risky as you approach your retirement date. This happens automatically, you do not have to choose individual stocks or bonds.

L-FUND (Income): The L Income Fund is designed for participants who are already retired or very close to retirement and are looking for a conservative and stable investment option that provides income in retirement.

Voluntary Retirement Savings: The TSP allows eligible participants to voluntarily contribute a portion of their salary toward their retirement savings. Contributions are made on a pre-tax or Roth basis, providing participants with options for reducing their current taxable income or potentially receiving tax-free withdrawals in retirement.

Tax-Advantaged Savings: Contributions to the traditional TSP are tax-deferred, meaning you don't pay taxes on the contributions or any investment earnings until you withdraw the funds in retirement. Roth TSP contributions are made with after-tax dollars, and qualified withdrawals in retirement are tax-free.

TSP Investment Funds: The TSP offers a selection of low-cost investment funds, including both individual funds that cover different asset classes (such as stocks, bonds, and government securities) and Lifecycle Funds (L Funds) that automatically adjust the investment mix based on your expected retirement date. The different funds vary in levels of risk. The funds are listed here in order, from least to most risk: G, F, C, S & I

Click to enlarge TSP Match Chart

About the TSP funds

TSP funds matching

More TSP features

Key health benefits available in FERS retirement

Federal employees who retire are eligible for health benefits coverage through the Federal Employees Health Benefits (FEHB) Program, provided they meet certain criteria. The FEHB Program offers a variety of health insurance options to choose from.

The government health plan is among the best in the nation because of the variety of options you have to choose fro each year and the fact that they subsidize your premiums by 72% for life!

What FERS health benefits are available in retirement?

Federal Employees Health Benefits (FEHB) Program: The FEHB Program provides comprehensive health insurance coverage for federal employees, retirees, and their eligible family members. Retirees can continue their FEHB coverage into retirement as long as they were enrolled in the program for the five years leading up to their retirement date, or if they were covered under another qualifying health plan.

Choice of Health Plans: The FEHB Program offers a wide range of health insurance plans, including fee-for-service plans, health maintenance organizations (HMOs), and high-deductible health plans with Health Savings Accounts (HSAs). Retirees can choose the plan that best suits their healthcare needs and preferences.

Continued Premium Payments: Retirees must continue to pay their share of the health insurance premium, just as they did while working. However, these premiums are generally lower than those in the private sector due to the group purchasing power of the federal employee pool.

Family Coverage: FEHB plans often offer family coverage options, allowing retirees to extend health benefits to their eligible family members, including spouses and dependent children.

Prescription Drug Coverage: Many FEHB plans provide prescription drug coverage, helping retirees manage their medication costs.

Dental and Vision Coverage: While dental and vision coverage is not included in the standard FEHB plans, some plans offer these options as part of their benefits package. Alternatively, retirees can choose separate dental and vision plans.

Flexible Enrollment: Retirees have the flexibility to change their FEHB plan during Open Season, which typically occurs annually. This allows retirees to adjust their coverage based on changing healthcare needs.

Medicare: All federal employees were required to begin paying into Medicare in March of 1986. That means even if you are CSRS you should be covered. Medicare coverage begins at age 65. You can sign up beginning 3 months before your 65th birthday, the month of your 65th birthday and 3 months after your 65th birthday to enroll (7 months total). There are 4 components to Medicare - Part A, Part B, Part C and Part D. For a brief overview of these components please see our article: Medicare: A Simple Explanation of the Costs and Components

Medicare (The mega short explanation):

Medicare Part A (Hospital Insurance): Covers inpatient hospital care, skilled nursing facility care, hospice care, and some home health care.

Medicare Part B (Medical Insurance): Covers outpatient services, doctor's visits, preventive care, diagnostic tests, and durable medical equipment.

Medicare Part C (Medicare Advantage): Offers comprehensive coverage through private insurance plans approved by Medicare, often including Parts A, B, and D benefits.

Medicare Part D (Prescription Drug Coverage): Provides prescription drug coverage through private insurance plans.

It's important for federal employees to carefully review the FEHB options available and select a plan that aligns with their healthcare preferences and needs. Before making any decisions, it's recommended to review plan details, premiums, coverage, and network providers. Additionally, retirees should consider the potential impact of Medicare eligibility on their healthcare coverage and costs, as Medicare can coordinate with FEHB coverage for retirees who are eligible for both programs.

Social Security & FERS, a brief history

When you retire under FERS, you'll receive a FERS annuity and Social Security benefits. Your FERS annuity is based on your federal service and contributions, while your Social Security benefits are based on your overall work history. To be eligible for Social Security retirement benefits, individuals generally need to have earned enough "credits" by working and paying Social Security taxes.

How does Social Security work with FERS?

Social Security was designed make up 20-30% of your retirement income. FERS is the other 20-30% and your TSP another 20-30%. These components combined can make up 60-90% of your working salary if utilized properly.

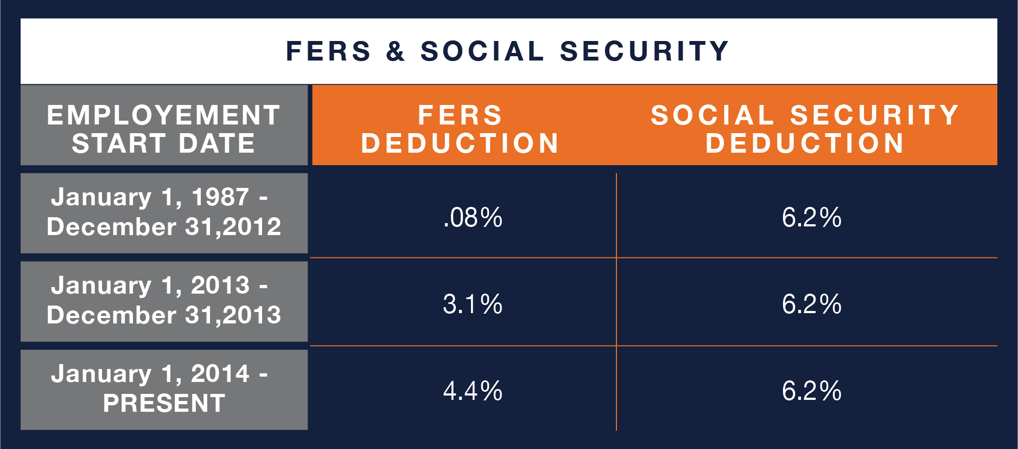

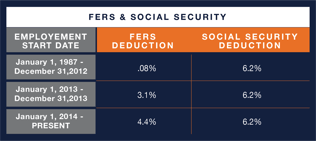

Prior to the FERS, federal employees worked for the CSRS or Civil Service Retirement System. The CSRS was designed to replace 80% of the employee's working salary. Employees did not pay into or receive any Social Security retirement benefits. The government soon saw that they were on the hook for a huge retirement payout so they decided to shift to a system like the 401k, which required employees to fund a larger portion of their own retirement. So they created the FERS and by January 1, 1987 it was in full swing. All federal employees between January 1, 1987 to December 31, 2012 contributed .08% of their salary to their own pension and 6.2% to Social Security. Beginning January 1, 2014 to present FERS employees must contribute 4.4% of their salary to their own pension and are still required to contribute 6.2% to Social Security.

The role of Social Security in your retirement from FERS

Quick Review: If you're covered by the Federal Employees Retirement System (FERS), you contribute a portion of your salary to Social Security, just like employees in the private sector. The Social Security tax rate is consistent regardless of whether you're covered by FERS or not.

The Social Security tax rate is 6.2% of your gross salary, up to a certain income limit (known as the Social Security wage base). This means that the maximum amount of your salary subject to the Social Security tax is capped each year. If your total annual salary exceeds the wage base, you won't pay Social Security taxes on the amount above that limit.

Keep in mind that tax rates and income limits can change over time due to updates in tax laws and regulations. Therefore, it is recommend that you check with your HR department or the Social Security Administration for the most up-to-date information on Social Security tax rates and wage bases.

Click to enlarge

FERS Special Provisions

Yes, there are special retirement provisions for certain categories of high-risk employees under the Federal Employees Retirement System (FERS). These provisions are designed to address the unique circumstances and challenges faced by individuals who work in high-risk occupations that may involve exposure to hazardous conditions, physical demands, or other factors that could impact their health and well-being over time.

Are there Special FERS Retirement Provisions for high-risk employees?

Law Enforcement Officers (LEOs): Law enforcement officers, including federal agents, park rangers, and other similar positions, have special retirement rules. They can retire earlier than regular FERS employees and are eligible for enhanced retirement benefits based on their service. LEOs who meet specific criteria can retire at age 50 with 20 years of service or at any age with 25 years of service.

Firefighters: Firefighters, including federal firefighters, have their own set of special retirement rules. Similar to LEOs, firefighters can retire earlier than regular FERS employees and receive enhanced retirement benefits. Qualified firefighters can retire at age 50 with 20 years of service or at any age with 25 years of service.

Air Traffic Controllers: Air traffic controllers also have special retirement provisions. They can retire at age 50 with 20 years of service or at any age with 25 years of service. These provisions recognize the high-stress nature of air traffic control positions.

Customs and Border Protection Officers (CBPOs): Customs and Border Protection Officers have specific retirement rules that allow them to retire earlier than regular FERS employees. CBPOs can retire at age 50 with 20 years of service or at any age with 25 years of service.

It's important to note that the specific requirements and benefits associated with these special retirement provisions may vary, and eligibility criteria are subject to change. If you are in a high-risk occupation covered by one of these special provisions, it's recommended that you consult with your agency's HR department, OPM or a certified Federal Retirement Consultant (FRC) for detailed and up-to-date information on retirement eligibility and benefits for your specific role. Click here to set a free consultation with a Legacy Retirement agent.

Basics of employee survivor benefits

FERS survivor benefits are designed to provide financial support to the surviving family members of federal employees who pass away. These benefits help ease the financial burden on the family during a difficult time.

It's important to note that survivor benefits under FERS can vary based on individual circumstances, including the length of federal service, marital status, and specific details of the employee's situation. Below is a simplified explanation of survivor benefits. For a more in-depth look at these benefits see our article, "FERS Survivor Benefits".

Survivor benefits are not the same as life insurance benefits. For an in-depth look at the life insurance provided to federal employees please see our article 'What is FEGLI & How Does it Work?'.

What are the Survivor Benefits Under FERS?

Basic Employee Death Benefit (BEDB): This is a lump-sum payment equal to the employee's final salary, plus a percentage based on years of federal service. The percentage varies depending on whether the employee had less than 10 years of service, between 10 and 14 years, or 15 or more years.

FERS Annuity for Spouse: The surviving spouse of a FERS employee may be eligible to receive an annuity, which is a monthly payment based on the employee's service and contributions to the FERS system. The annuity amount is typically 50% of the employee's unreduced annuity.

FERS Annuity for Dependent Children: Dependent children of a deceased FERS employee may also be eligible to receive an annuity until they reach a certain age or status. The amount is typically calculated as a percentage of the employee's unreduced annuity and may be shared among multiple children.

Special Survivor Benefits (SSB): In certain circumstances, if the employee was killed while performing their federal duties or if their death resulted from injuries sustained in the line of duty, the surviving spouse might receive an annuity that is higher than the standard annuity.

Applying for benefits

Contact the personnel office of the Federal agency where the employee worked. You should complete the Application for Death Benefits, Standard Form (SF) 3104(PDF file) and attach any other forms and/or evidence as the application or circumstances require. Attach a copy of the employee’s death certificate and a copy of the certificate of the marriage to the widow or widower. Give the application to the personnel office. If you are the surviving spouse or former spouse, you and deceased person’s employing agency should also complete Form (SF) 3104B(PDF file) Standard Documentation and Elections in Support of Application for Death Benefits when Deceased was an Employee at the Time of Death. A widow or widower who is claiming benefits for himself/herself and on behalf of children should file one application.

Again, it is important to note that the specific requirements and benefits associated with survivor benefits may vary, and eligibility criteria are subject to change. Additionally, the information on this page is not exhaustive. If you are in the circumstance where you are in need of applying for survivor benefits, it's recommended that you consult with your agency's HR department, OPM or a certified Federal Retirement Consultant (FRC) for detailed and up-to-date information.

Two main types of disability retirement

Yes, the Federal Employees Retirement System (FERS) does have special disability retirement options for federal employees who become disabled and are unable to continue working in their current capacity. FERS provides disability retirement benefits to eligible employees who meet certain criteria. There are two main types of disability retirement under FERS.

Does FERS have special disability retirement options?

Immediate Disability Retirement: This option is available to employees who have completed at least 18 months of federal civilian service and who are unable to perform their job duties due to a medical condition. To qualify, the medical condition must be expected to last at least one year. Immediate disability retirement provides an annuity that is computed in a manner similar to regular FERS retirement but uses the employee's actual service up to the date of disability.

Deferred Disability Retirement: If you have less than 18 months of federal service, you may still qualify for deferred disability retirement. This means that your application will be postponed until you have completed 18 months of service. Deferred disability retirement follows the same eligibility criteria and computation methods as immediate disability retirement.

It's important to note that the disability retirement process involves several steps, including medical evaluations and assessments by the Office of Personnel Management (OPM). The medical condition must be documented and supported by medical evidence. OPM reviews the medical evidence and determines whether the disability meets the eligibility requirements for FERS disability retirement.

If you believe you may be eligible for FERS disability retirement, it's recommended to contact your agency's human resources department and review the information provided by the Office of Personnel Management for detailed guidance and instructions on how to apply. Keep in mind that the above information is based on knowledge available at the time of its writing, there might have been changes or updates since that time. For the most current and accurate information, refer to official government resources or contact the appropriate authorities.

Take your time, you have many options!

When contemplating the climb a massive mountain like Mt. Everest, most initially only think about the climb - getting there! Once at Everest Base Camp, it then takes an average of 40 days to climb to the peak of Mt. Everest. Few realize that It can take a few days or a week to descend, from the summit. Climbers must be extra cautious, in either the climb or the descent - following an experienced guide is essential for survival.

Your progression to retirement is much the same. Planning for retirement day is a career-long trek for which you seek guidance from financial professionals to multiply and protect your savings. However once you reach the peak of your career, aka retirement, it is wise to seek the assistance of an experienced guide to help you navigate the exit process of the FERS including timing, paperwork and choosing the correct options that fit your unique circumstances. To that end, here are some practical suggestions:

Where can I find help to plan for my retirement from FERS?

There is no sense in rushing into a decision. Often times people work with a financial planner for decades - right on thru retirement. This is a long term relationship and there are many financial agents to choose from. You should feel comfortable and be put at ease by your interaction with the financial agent you choose. Look for a financial professional who is attentive, listens to your concerns, and takes the time to explain complex financial concepts in a way that you can understand. Check references, reviews and credentials to be sure you are working with an individual or agency that will put your needs first.

Use a certified Federal Retirement Consultant (FRC)

The Federation of Federal Employee Benefit Advocates, LLC (“FFEBA”) educates and certifies professionals who work with federal employees. The Federal Retirement Consultant℠ designation applies to professionals who are able to demonstrate their competence and knowledge of federal employee retirement systems and related benefits. In order to obtain and maintain the FRC℠ certification, individuals are required to demonstrate a commitment to high standards, continuing education, professional ethics, and trust.

Know before you go...

Know your needs before meeting with an advisor. Take some time to identify your financial goals & retirement needs. For example, you could take the five needs of retirement and place them in order of importance to you. The needs we are referring to are: Stability, Income, Growth, Death Benefit & Liquidity. Rank these five things in order of their importance to you. Then share that information with the financial agent of your choice. Understanding your needs will help you and your advisor to find a plan of action that is most relevant to your unique circumstances. Good communication is essential to a successful plan!

Would you welcome a free retirement plan?

Are you ready to take charge of your retirement future? We invite you to schedule a complimentary appointment with us to delve into your individual retirement aspirations and needs. Our team is dedicated to understanding your unique situation and tailoring a personalized plan just for you – all at no cost. Let's work together to ensure your retirement dreams become a reality.

Planning for your retirement may be the most important financial decision of your life. Helping you would be a tremendous honor.

- Legacy Retirement

Disclaimer

The intent of this website is to simplify the complex, complicated and sometimes confusing explanations that often accompany tax codes, pension standards or other financial jargon. In no way does LegacyRetirementGoals.com claim ownership or otherwise claim to be the express authority on any stated subject matter on any page or blog produced and shared on this site. Further, LegacyRetirementGoals.com, it's owners and/or affiliates do not work for TSERS, FERS or any other government agency. It's important to note that the eligibility requirements for TSERS, FERS or other referenced retirement benefits may change over time due to legislative changes or updates in the retirement plan rules.